A polyurethane foam plant manager in India opens her inbox to find a force majeure notice from a regional MDI supplier the third this quarter. Outside Jebel Ali, dozens of tankers sit idle, their cargo holds empty, waiting for a waterway that has effectively been closed for over three months. For chemical buyers across the polyurethane value chain, this isn't an abstract geopolitical headline anymore. It's a line item that just got 40% more expensive.

What Happened Exactly?

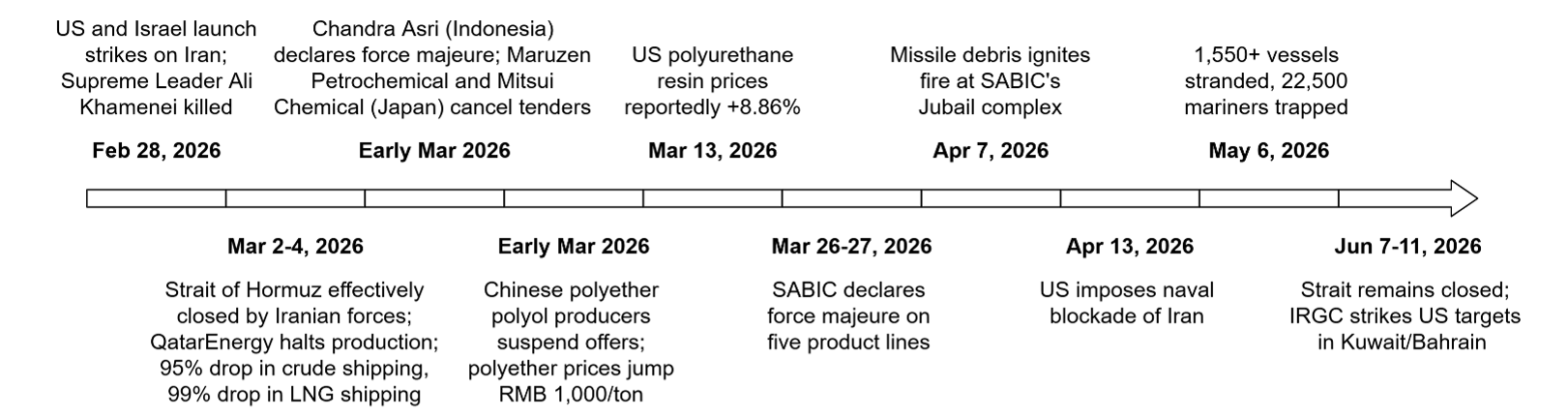

On February 28, 2026, US and Israeli forces launched strikes on Iran. Within days, Iranian forces effectively closed the Strait of Hormuz the corridor through which roughly a fifth of the world's oil and LNG normally moves. According to World Trade Organization data cited in a House of Commons Library briefing, shipping through the strait collapsed by 95% for crude oil and 99% for LNG. A US-led campaign to reopen the strait began in mid-March, followed by a naval blockade of Iran from April 13. As of early June, the strait remains effectively closed to commercial traffic, with live tracking services reporting transit volumes still running at a small fraction of the pre-war baseline. For chemical buyers tracking MDI price increase 2026 trends, this single chokepoint event is the root cause of nearly everything that follows.

100+ Days That Shook the Polyurethane Market

Source: Secondary & Primary Research and Prismane Consulting Estimates

The 1.9 Million Ton Problem

More than 1.9 million tons of global MDI capacity were simultaneously affected during Q1-2026 alone an unprecedented, synchronized supply shock and a key driver behind the broader MDI price increase 2026 trend. There have been cumulative price increases for both Polymeric MDI and Monomeric MDI that have approached 40% since January 2026, with no clear sign of retreat. TDI, flexible foam polyether polyols, and TPU have each climbed more than 20% over six months, while CASE polyether polyols are up nearly 30%. This is TDI supply chain disruption and MDI price increase 2026 happening at the same time, across the same feedstock pool which is precisely why isocyanate market 2026 conditions look so different from a typical seasonal tightening.

In India specifically, data shows TDI prices climbing roughly 53% and polymeric MDI roughly 65% since early March, with flexible slab stock polyols up around 74% a vivid illustration of how Strait of Hormuz polyurethane disruptions cascade fastest into import-dependent markets.

TDI Monthly Price Movements, November 2025 to May-2026

Source: Secondary & Primary Research and Prismane Consulting Estimates

PMDI Monthly Price Movements, December 2025 to May 2026

Source: Secondary & Primary Research and Prismane Consulting Estimates

Why Saudi Arabia and the GCC Matter to Your Isocyanate Supply

Isocyanate production starts upstream naphtha cracking feeds benzene and propylene oxide (PO), the building blocks for aniline and ultimately MDI and TDI. GCC petrochemicals producers like SABIC, Sipchem, and Equate sit at the heart of this naphtha-to-PO chain, and Middle East petrochemical disruption has hit them directly. SABIC declared force majeure on several product lines out of its Jubail complex following Hormuz-related shipping disruptions, and a missile strike on April 7 caused a fire at the Jubail industrial complex itself. Separately, SABIC's large methanol plant at Jubail went fully offline under force majeure, compounding a regional methanol shortfall already running above 20%. The disruption isn't confined to one producer, either as Sadara Chemical the Aramco-Dow joint venture also based in Jubail, with annual capacity exceeding 3 million tons of chemicals and plastics temporarily halted all production on March 31, citing ongoing supply chain disruptions and offering no timeline for restart. With naphtha supply from the Gulf constrained, Asian crackers the next link feeding aromatics into MDI and TDI production are running short of feedstock, regardless of whether their own plants are operational.

Ships anchored near the Strait of Hormuz during the 2026 MDI price increase crisis

Source: BBC and Marine Traffic/Kpler

What This Means for Buyers Right Now

The practical signals are already visible. Indonesia's Chandra Asri declared force majeure across all contracts, while Japanese buyers Maruzen Petrochemical and Mitsui Chemical cancelled second-half-April naphtha import tenders, according to Reuters reporting. Asian naphtha refining margins hit a four-year high. In the US, producers including Covestro and Huntsman have layered fresh outages a Covestro Baytown force majeure and Huntsman Geismar maintenance, both running June 1-10 onto an already-tight North American market where a handful of producers control the vast majority of capacity.

For buyers, three things follow, expect continued upward pressure on contract negotiations through Q3; build in longer lead times given Cape of Good Hope re-routing (adding 10–14 days and emergency surcharges of up to $2,000/container); and treat force majeure notices from any GCC or Asia-linked supplier as a near-term certainty rather than a tail risk.

Coming Next

“Polyether Polyols Price Middle East Conflict: The Quiet Casualty Reshaping Global PU Supply” Blog in this series traces the ripple effect downstream into polyether polyols and the broader PU value chain including foam, coatings, adhesives, and elastomers. For a full plant-by-plant capacity breakdown and MDI price increase 2026 price forecast through 2027, Prismane Consulting’s Global MDI & TDI Market: Geopolitical Risk Assessment 2026 report is available here: [link].