Engineering Plastics Market Overview

With its remarkable physical and mechanical properties, Engineering Plastics have increasingly cemented their position as substitutes for metals in many huge strength applications. Engineering Plastics provide good mechanical strength combined with great dimensional stability. They also possess good creep and fatigue resistance. They are tough materials having low coefficient of friction. These properties make Engineering Plastics suitable for various precision applications. Engineering Plastics has a wide spectrum of applications in automotive, electrical & electronics, industrial machinery, consumer products, medical devices, sporting goods and other emerging applications.

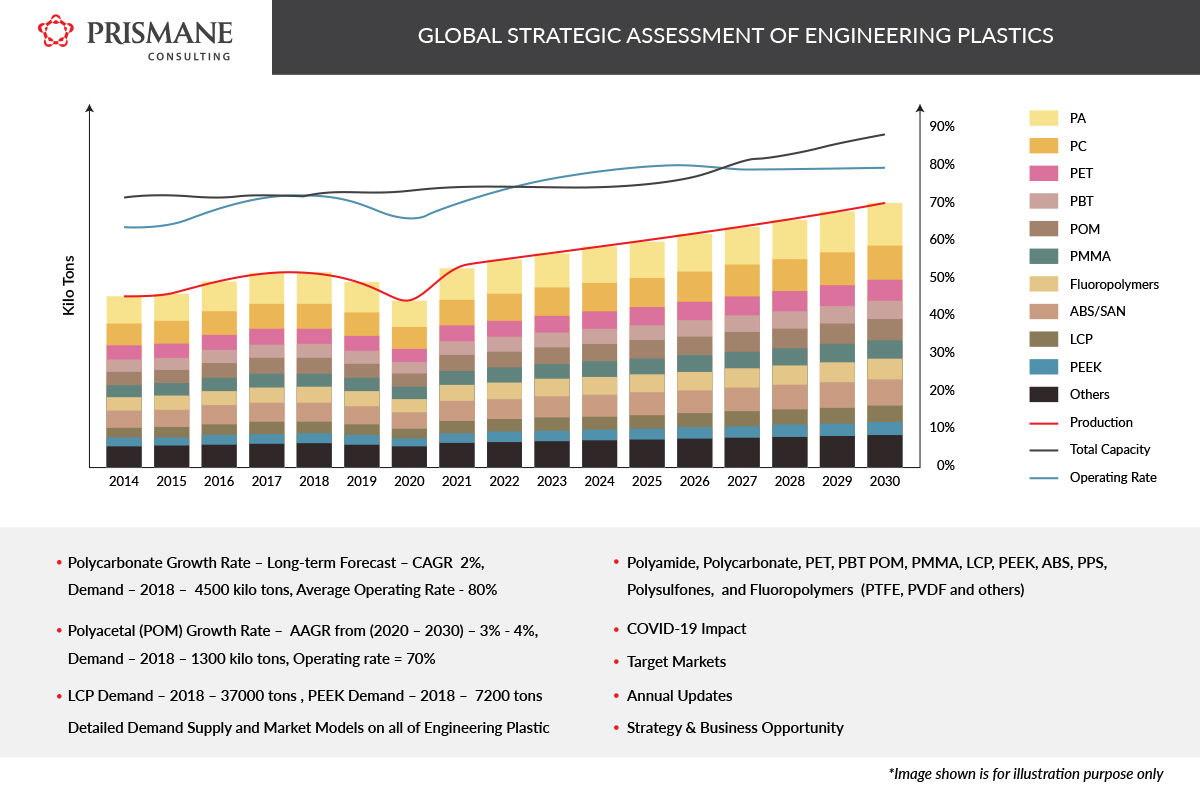

Global Engineering Plastics Market Trends

The global engineering plastic market has shown higher growth rates largely driven by rising demand from engineering plastic end-users in China and other Asian countries. Historically, economically mature regions like North America and Western Europe have witnessed below-average growth rates and will continue to lose their demand market share to Asia-Pacific.

Regional Outlook for Engineering Plastics

Engineering plastics consumption is mostly well above the global GDP growth. In the long-term forecast, it is expected to continue this trend. Growth is forecast to remain high in all regions, benefiting from increased market penetration in addition to overall sector growth. Engineering plastics growth is expected to be higher in Asia-Pacific and Central & Eastern Europe. Asia-Pacific regional demand growth will drive the global engineering plastics market.

The market for engineering plastics is dominated by packaging, which accounts for close to 50% of demand globally. Packaging applications include food and other consumer uses to industrial applications. Packaging application consumes major part of PET demand. Demand for engineering plastics is followed by electrical and electronics and automotive application.

Historically, the demand growth in the packaging application has seen fast growth and most of this has been PET. Polycarbonate market has witnessed faster growth rate than other types, driven by its superior mechanical properties as it provides better stiffness-to-toughness balance in comparison to other plastics.

Impact of Covid-19 on Engineering Plastics Industry

The COVID 19 pandemic has significantly impacted the integrated automotive industry not only in China but also in USA, Europe, and other Asian countries. The pandemic has had some long-term impacts on the automotive sector owing to repeated regional lockdowns that had severe effect and implications on labour, capital, and productivity.

The anticipated growth of the packaging and automotive industry in Asian countries and increase in vehicle sales projections in Europe is expected to drive the global engineering plastics industry. The overall drivers for all major engineering plastics though remain same – they are all driven by the increase in demand for consumer durables.

The major drivers of engineering plastic include the slow growth of packaging industry and metal replacement properties and tightening of emission standards in the automotive sector. The impact of the pandemic on the packaging sector has been mixed. The demand for packaging in healthcare sector increased the while positive demand was also witnessed in food & beverages and other groceries. The demand in luxury packaging and automotive transportation declined and it still faces a lot of challenges owing to the Pandemic.

Outlook for the Automotive Industry

The automotive industry is forecast to grow at a slower pace in all major regions owing to the retrival in automotive demand and Government backed incentives like EU Recovery Fund and EU Green Deal. The growing confidence because of increased vaccinations, decline in COVID 19 cases and ease of restrictions is expected to increase the production and sales of automotive, electronic products and other consumer goods. The market is believed to remain subdued during the short-term forecast until 2024 because of long-term remote working and bleak economy.

The consumer electronics industry was impacted due to the COVID 19 pandemic while one of the most-hard hit sectors was industrial manufacturing, especially where remote working was not possible. Many organisations had to stop their operations in the first half of 2020 owing to continued downward pressure on demand, production, and revenues.