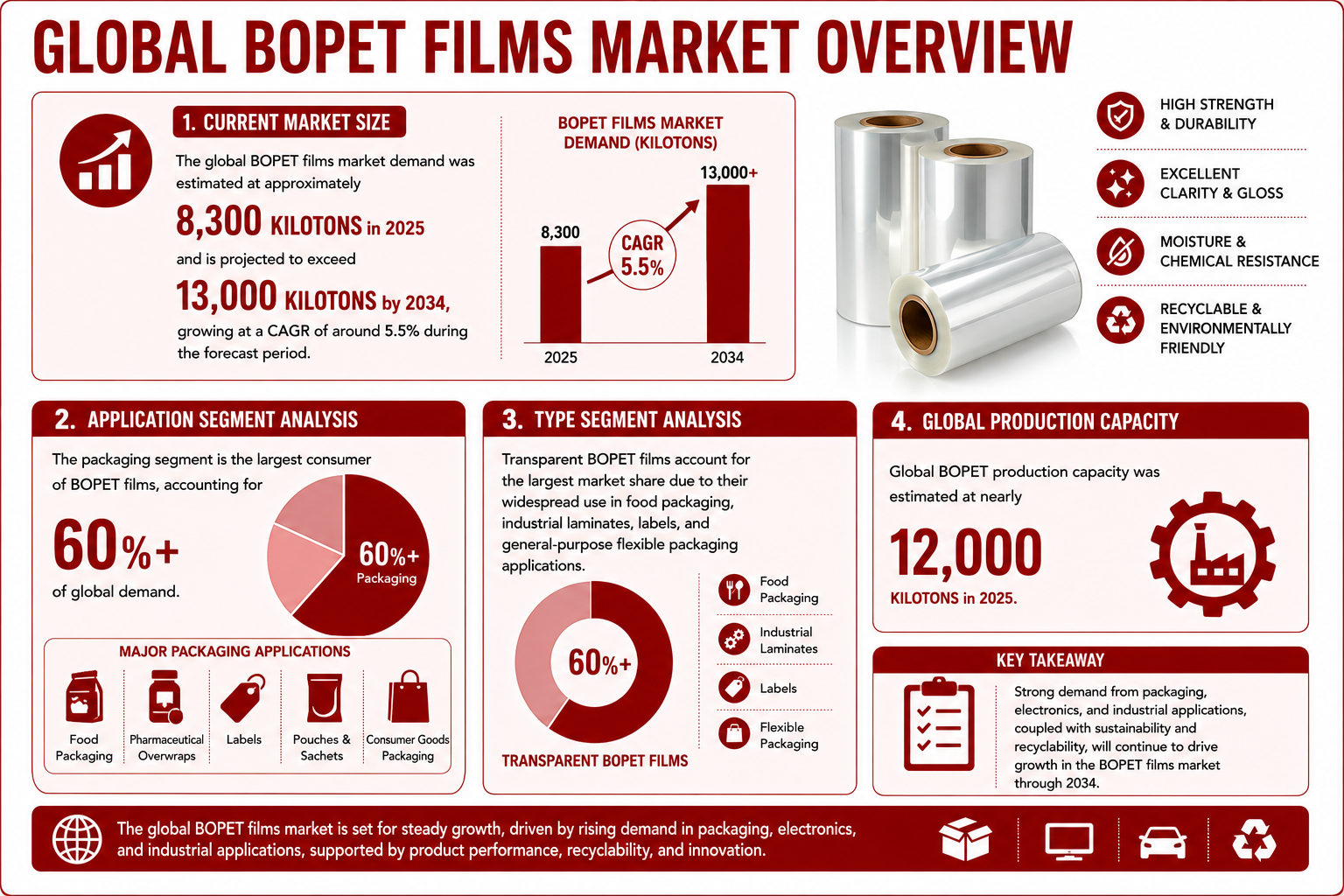

The global BOPET Films market size was estimated to be around 8,300 kilo tons, and it is projected to register a CAGR of 5.5% during the forecast period to cross 13,000 kilo tons by end of 2034. This strong growth is mainly fueled by the increasing use of BOPET films in various sectors, including food and beverage, pharmaceuticals, personal care and cosmetics, electronics, among others. BOPET films are widely adopted in these industries owing to their ability to protect products from UV radiation, oxygen, and moisture, while also offering excellent printability and mechanical performance. As global demand for flexible packaging and sustainable materials continues to rise, the BOPET market is undergoing transformation. While BOPET consumption remains robust, particularly in Asia-Pacific, aggressive capacity expansions have intensified competition and placed pressure on margins across commodity-grade products.

BOPET Films Market Demand, 2018-2034 (kilo tons)

Source: Secondary & Primary Research and Prismane Consulting estimates

Factors Influencing BOPET Market:

Packaging industry shift from rigid packaging to flexible packaging

A shift has been made from rigid packaging to flexible packaging in the global packaging industry with an emphasis on cost efficiency, improved logistics, and sustainability. The evolution of these structures greatly affects the market for BOPET films, as flexible packaging demands materials with high dimensional stability, superior printability, and strong barrier properties all attributes of BOPET films. Furthermore, BOPET films provide high mechanical strength at low thickness and allow downgauging without compromising performance. This feature aids in material reduction, cost optimization, and achieving sustainability, reinforcing the growth of BOPET films in flexible packaging applications.

Increase in demand for high barrier and premium packaging formats!

Market demand for high barrier and premium packaging formats like metallized and coated BOPET films for extended shelf life and product protection applications is emerging in addition to the growing materials and technology with which a wide variety of advanced BOPET films needs to be produced. The latest developments in film coatings, surface treatment, and downgauging are driving the increasing needs for specialty BOPET films in films.

BOPET Supply Analysis

The global BOPET production capacity was estimated at nearly 12,000 kilo tons in 2025, representing growth from 7,200 kilotons in 2018. The BOPET market has witnessed strong capacity addition over the past decade, largely driven by rising demand from the flexible packaging, electronics, and industrial sectors. Asia-Pacific remains the dominant global BOPET supply hub, accounting for the majority of installed BOPET capacity, followed by North America and Europe. The region is also estimated to capture most of the announced capacity additions during the forecast period, reinforcing its position as the center of global polyester film production.

Within Asia-Pacific, China and India emerged as the leading BOPET producers in 2025, supported by strong domestic demand, competitive manufacturing costs, integrated supply chains, and export-oriented production strategies. China continues to benefit from its large packaging and electronics industries, while India has rapidly strengthened its position as a major global supplier through sustained investments in new production facilities.

On the demand side, Asia-Pacific is the fastest-growing BOPET market in absolute terms, fueled by rising disposable incomes, rapid urbanization, expanding organized food retail, increasing consumption of packaged foods, and continued growth in electronics manufacturing across China, India, and Southeast Asia. India, in particular, has experienced notable capacity growth, with several new BOPET production lines commissioned by leading manufacturers such as Ester Industries, Cosmo Films, UFlex, and Chiripal. These investments are aimed at meeting both robust domestic consumption and growing export demand, further solidifying India's role in the global BOPET value chain.

BOPET Market, by Type

Based on type, BOPET market is analyzed across transparent films, metallized films, coated films, laminated films, and speciality films. BOPET films demand is driven by the functional requirements of flexible packaging and technical applications, with transparent BOPET accounting for the largest share due to its widespread use as a base film in food packaging, labeling, and industrial laminates where high clarity, printability, and mechanical strength are essential.

Metallized BOPET film is a rapidly growing market based on the growing need of high-barrier and decorative packaging for snacks, confectionery, coffee, and personal care, leading to enhanced oxygen and moisture barrier performance due to being lightweight and cheaper than aluminum foil.

Coated BOPET films, such as barrier-coated, corona-treated, heat-seal, or UV-coated plastics of packaging films, are increasingly attractive as brand owners desire improved sealing and surface adhesion, as well as for performance in high-speed and quality packing. Laminated BOPET films are increasing steadily on account of their contribution as a structural layer in the multilayer flexible packaging; they enhance the durability as well as the dimension stability of the pouches, sachets, and pharmaceutical overwraps. Functionalized BOPET films, containing flame-retardant, anti-fog and anti-static variants, occupy a relatively small, high-value, niche driven by a set of tailored conditions in electronics, industrial and fresh food packaging applications.

BOPET Films Demand, By Type, 2025 (kilo tons)

Source: Secondary & Primary Research and Prismane Consulting estimates

BOPET Film Market, by Application

Based on application, the market is segmented across packaging, electrical & electronics, solar & photovoltaic, imaging, industrial applications, and others. Packaging segment accounts the largest share due to extensive use in flexible food packaging, pharmaceutical overwraps, labels, and consumer goods packaging, where high strength, printability, and better barrier performance is required.

Packaging remains the largest end-use segment for BOPET films market, accounting for more than 60% of global demand. Food manufacturers increasingly rely on BOPET-based laminates for snacks, confectionery, dairy products, frozen foods, and ready-to-eat meals due to their excellent oxygen and moisture barrier characteristics. The growth of e-commerce and changing consumer lifestyles have further accelerated demand for convenient and lightweight packaging solutions.

Electrical & electronics represent significant market share in the consumption of BOPET film. The demand for BOPET films in this segment is mostly driven by the presence of insulation property of the BOPET films which can be utilized for flexible circuits and capacitor films that require high dielectric strength and thermal stability.

Solar & photovoltaic industry application is an emerging hotspot for BOPET films market demand growth. The demand for BOPET film in this application is mostly due to increase in the usage of films in back sheet and protective layers due to their durability and weather resistance.

Imaging applications including graphic and industrial imaging films, continue to generate steady demand supported by their dimensional stability and optical clarity. Industrial applications, such as labeling, laminates, and insulation, contribute consistent volume demand, while other applications, including automotive, aerospace, and specialty coatings, remain niche but high-value segments driven by performance-critical requirements.

BOPET Films Demand, By Application, 2025 (kilo tons)

Source: Secondary & Primary Research and Prismane Consulting estimates

BOPET Films Market, by region

By region, BOPET films demand is analyzed across North America, Europe, Northeast Asia, Southeast Asia, Indian Subcontinent, Middle East, Rest of World. Northeast Asia accounts for the largest share of global BOPET demand, estimated at around one-third of total consumption, driven by its strong manufacturing base, high concentration of packaging converters, and large-scale electronics and industrial production. Europe represents the second-largest regional market, supported by widespread adoption of high-barrier and sustainable packaging solutions, stringent regulatory standards, and steady demand from food, pharmaceutical, and personal care sectors. North America holds a significant but relatively mature share of demand, characterized by stable growth, high penetration of flexible packaging, and strong demand for premium and specialty BOPET films grades.

Indian subcontinent and southeast Asia are the fastest-growing regions, supported by rapid urbanization, expanding packaged food consumption, rising pharmaceutical manufacturing, and increasing investments in flexible packaging capacity; together, these regions are gaining share from more mature markets.

BOPET Films Demand, By Region, 2025 (kilo tons)

Source: Secondary & Primary Research and Prismane Consulting estimates

Competitive Landscape

Top players analyzed in BOPET market is Toray Industries, UFLEX Limited, Polyplex, SRF Limited, Jindal Poly Films Limited, Mylar Specialty Films, Mitsubishi Polyester Film GmbH, SKC, Vacmet India Limited, Cosmo First Limited. In addition to the abovementioned players, we have also analyzed Ester Industries Limited, Gettel High-Tech Materials Co., Ltd., Chiripal Poly Films, Polinas, Oben Group, and Others.

Key Developments

- In December 2024, Uflex Limited committed an investment of 200 million USD in Egypt to strengthen backward integration and broaden its market presence. Of this amount, 70 million USD was designated for the establishment of a PET chips facility, which is essential for producing BOPET films utilized in flexible packaging manufacturing.

- In November 2024, Polyplex increased resin capacity to 86 KT in Decatur, Alabama facility which reduced PET film lead times in the US.

- In February 2024, Mitsubishi Polyester Film GmbH is construction a new PET film Plant in Germany with a capacity of 27 KT of HOSTAPHAN films.

- In December 2022, Toray Industries, Inc. introduced a sustainable PET film that offers enhanced adhesion and compatibility with water-based and solvent-free coatings.

- In April 2022, Jindal Polypack, part of Jindal Poly Films Limited, purchased the entire ownership of SMI Coated Products.