Europe's packaging rulebook has changed. The Packaging and Packaging Waste Regulation, Regulation (EU) 2025/40, better known as PPWR, entered into force in February 2025 and becomes applicable across all 27 member states from 12 August 2026. Unlike the directive it replaces, PPWR applies directly and uniformly, with no national transposition and no grace period. From that date onward, packaging placed on the EU market must satisfy a new set of sustainability, documentation, and design obligations.

For the flexible packaging industry, however, the date that matters most sits a little further out. From 1 January 2030, packaging must achieve a recyclability performance grade of A, B, or C to remain on the EU market. Structures that cannot be recycled at scale within existing infrastructure will simply lose access to one of the world's largest consumer markets.

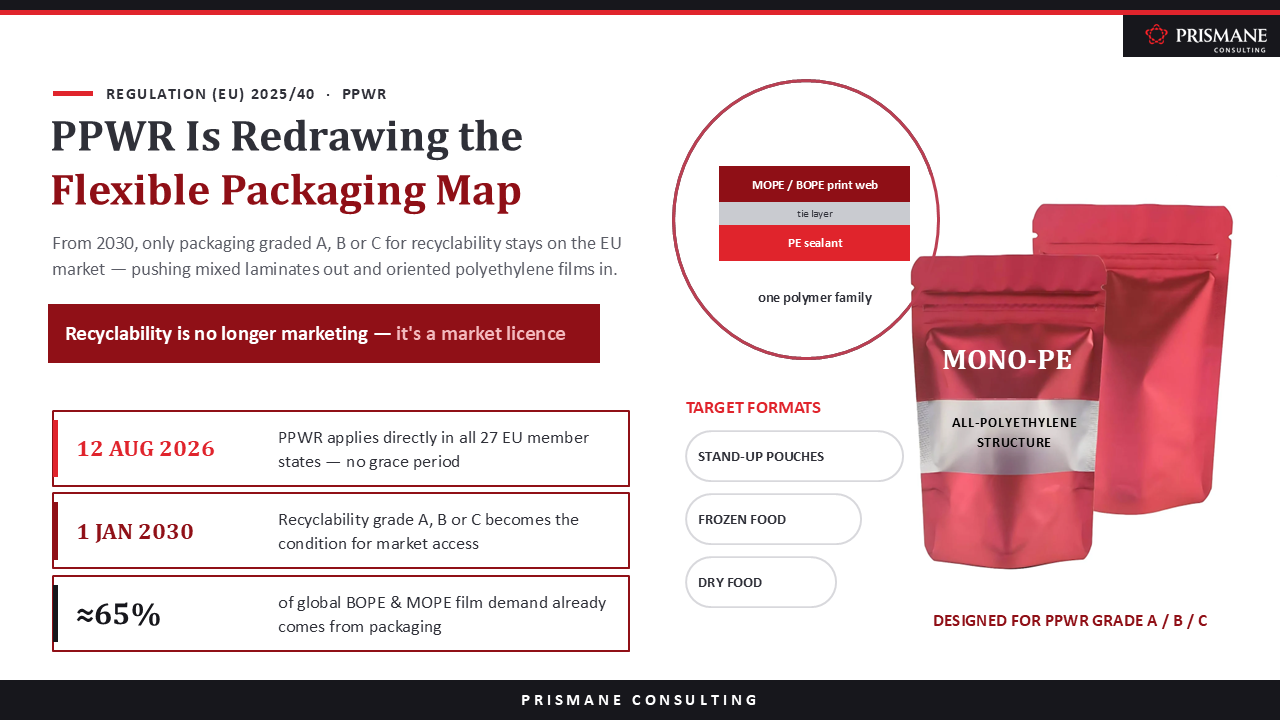

That single provision is set to reshape material selection across the flexible packaging value chain, and it puts oriented polyethylene films, BOPE and MOPE, directly in the spotlight.

The Structural Weakness of Today's Laminates

A large share of flexible packaging on shelves today is built from mixed polymer laminates. PET or nylon print webs are bonded to polyethylene sealant layers, often with EVOH or other barrier materials in between. Each layer earns its place on performance, providing stiffness for converting, barrier properties for shelf life, and sealability for filling lines. The difficulty arises at end of life. Mechanical recycling streams cannot separate these bonded, dissimilar polymers, which means the laminate is destined for landfill or incineration.

Under the old directive, that was a reputational issue. Under PPWR's recyclability grading system, it becomes a market access issue with a fixed deadline.

Where Oriented PE Fits In

The most practical route to compliance for many flexible packaging formats is to rebuild the laminate from a single polymer family. If every layer is polyethylene, the pack can flow through established PE recycling streams. This is precisely the role-oriented PE films are designed to play.

- BOPE (biaxially oriented polyethylene) is stretched in both the machine direction and the transverse direction, giving it balanced tensile strength, puncture resistance, good moisture barrier, and clarity. These attributes have made it a strong candidate for frozen food, dry food, and other demanding applications where PET or nylon webs were previously the default.

- MOPE (mono oriented polyethylene, also marketed as MDO PE or MDOPE) is stretched only in the machine direction, producing the directional stiffness and printability needed for the outer web of stand-up pouches and similar formats.

Paired with a PE sealant layer, either film enables an all-PE construction that can replicate much of the functionality of conventional mixed material laminates while qualifying for the recyclability grades PPWR demands.

Why Decisions Are Being Made Now, not in 2030

A 2030 deadline can sound distant. In flexible packaging, it is not. Requalifying a laminate involves film trials, printing and lamination adjustments, filling line validation, shelf-life studies, and supply agreements, a process that routinely consumes one to two years for each format. Brand owners intending to be compliant well before the grading cut off need their material decisions locked in during 2026 through 2028.

Two additional factors are compressing the timeline. First, the European Commission's implementation guidance and frequently asked questions, published in March 2026, resolved much of the interpretive uncertainty that had allowed companies to defer action. Second, EPR fee modulation under PPWR ties producer fees to recyclability performance, meaning poorly graded packaging becomes progressively more expensive to place on the market even before any outright restriction applies.

The result is a demand pull for oriented PE films that begins well ahead of the regulatory deadlines themselves.

The Market Picture

Prismane Consulting's BOPE and MOPE Market Demand & Forecast Analysis 2034 finds that packaging already accounts for roughly 65 percent of global demand for these films, with growth underpinned by the broader move toward lightweight, recyclable, high performance materials.

The study also identifies the constraints that will shape how quickly the transition unfolds. Oriented PE remains a young film category relative to BOPP and BOPET, with converting capacity still building out. Feedstock economics add another layer of uncertainty. Swings in crude oil and polyethylene resin prices flow directly into film costs and can complicate substitution decisions. Regional dynamics differ as well. Europe's regulatory pull contrasts with Asia's capacity led expansion, and the interplay between the two will determine where investment lands first.

The Bottom Line

PPWR has converted recyclability from a marketing narrative into a licensing condition for the EU market, with August 2026 as the starting point and January 2030 as the finish line for recyclability grades. For BOPE and MOPE, that regulatory architecture translates into a multiyear adoption runway, one in which film producers, converters, and brand owners that qualify solutions early will hold a structural advantage over those that wait.

Go Deeper

The BOPE and MOPE Market Demand & Forecast Analysis 2034 covers demand by type and application, sales and revenue, pricing analysis, country level market balances, competitive landscape, and business opportunity assessment across the 2018 to 2034 period.

📊 Explore the full report - https://prismaneconsulting.com/report-details/bope-and-mope-market

For bespoke analysis on oriented PE films, PPWR impact assessment, or sustainable packaging strategy, reach us at info@prismaneconsulting.com