As covered in “MDI Price Increase 2026”, the Hormuz closure triggered a roughly 40% surge in MDI and TDI prices. But isocyanates have been getting the headlines polyether polyols, the other half of every polyurethane formulation, have been moving just as sharply, just less visibly, and the regional pattern tells a more interesting story about where this market goes next.

The Regional Divergence Story

This is no longer a single global price shock it's three different markets reacting to the same root cause in three different ways, and that divergence is the core polyether polyols price Middle East conflict story for procurement teams right now.

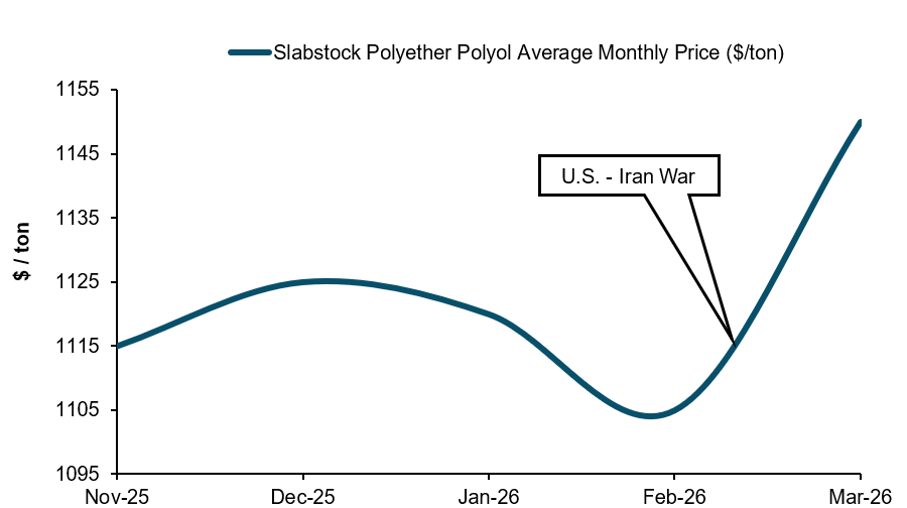

In Europe, there has been a €150/ton increase across all polyether polyol grades effective December 3, 2025, followed by a further €100/ton hike on February 27, 2026, both citing raw material, energy, and transport costs. This lands on an already-fragile European base flexible slabstock polyol spot price opened 2025 at €1,250/ton, spiked to €1,500/ton in April on seasonal restocking, then fell nearly 30% to a €1,000-1,060/ton trough by October as structural overcapacity and cheap Asian imports squeezed European producers. Dow's confirmed shutdown of its Tertre, Belgium facility (94 kilo tons/year of commodity capacity, ceasing by end-March 2026) had already stripped out shock-absorption capacity before Hormuz hit. Now energy-cost-exposed European producers are pushing increases into a market with less domestic supply cushion than it had a year ago a textbook case of polyether polyols price Middle East conflict dynamics meeting pre-existing structural weakness.

In Asia, the propylene oxide supply disruption angle dominates. China has expanded PO capacity by roughly 90% since 2021 and polyether capacity by 61%, according to industry reporting a "high-capacity, low-profit" structure that, in normal times, keeps a lid on prices. But in early March 2026, Chinese polyether producers suspended offers altogether as upstream PO costs jumped sharply within days, with the entire polyether product line posting gains of roughly RMB 1,000/ton in a single week. That's the China PO capacity paradox as the enormous nameplate capacity didn't prevent a supply scramble, because the shock hit feedstock costs faster than producers could reprice finished product.

In the Americas, the picture is starkly different. The US refinery utilization has held at average of 92.5% through May reaching 95.3% in June, and the 3-2-1 crack spread the standard refining-margin benchmark has surged from under $20/bbl at the start of 2026 to over $54/bbl as Gulf Coast refiners step into the gap left by disrupted Middle East supply. The US exported record 5.4 million b/d of crude oil over the four weeks ending May 1st, nearly matching imports for the first time in years. For polyol buyers, that's the Gulf Coast petrochemicals story in a nutshell while Europe and Asia scramble for feedstock, US producers are running near capacity and exporting aggressively making them a genuinely attractive near-term sourcing alternative, if freight costs are consumed by buyers.

Western Europe Flexible Slabstock Polyether Polyol Prices Nov 2025-Mar 2026

Source: Secondary & Primary Research and Prismane Consulting Estimates

Why Polyols and Isocyanates Move Together

Every PU system flexible foam for furniture and automotive seating, rigid foam for insulation, CASE formulations, and TPU for footwear requires both a polyol and an isocyanate in a defined ratio. A shock to either side of that ratio creates a bottleneck for the whole system. If your MDI supply tightens but polyol flows normally (or vice versa), you can't simply substitute your way around it without reformulating, which takes time most converters don't have. That's why this isn't really "two separate stories" it's one feedstock-integration problem with two price curves, and CASE polyols, which are facing a 30% price increase, sit squarely in the crossfire.

What Happens Next Three Scenarios

Scenario A, Hormuz reopens following diplomatic progress, flows resume gradually, and pricing eases toward something like the EIA's June 2026 outlook, which now assumes Brent averaging around $105/bbl through June-July, with Hormuz traffic resuming in Q3 and easing toward $79/bbl by 2027 a longer, slower normalization than earlier forecasts assumed.

Scenario B, prolonged closure, sustained risk premium, history offers two different templates here. The 1973 Arab oil embargo lasted only about six months but triggered years of structural realignment in global energy and chemical feedstock markets. The 1990 Gulf War shock, by contrast, was sharper oil roughly tripled within two months but normalized faster once Kuwait's production came back online. Which template applies to Hormuz depends on whether this is a short, sharp interruption or the start of a longer structural shift in Gulf supply reliability. Either way, in this scenario, polyol-isocyanate ratio bottlenecks persist well into 2027.

Scenario C, partial reopening with structural cost floor, even if physical flows resume, elevated insurance, war-risk premiums, and Cape of Good Hope rerouting keep freight-linked costs permanently higher than pre-crisis baselines a "new normal" floor under polyol pricing.

Plan Your Procurement Strategy

For a full regional breakdown of the polyether polyols price Middle East conflict story and forecast through 2027, see Prismane's Global Polyether Polyols Market: Regional Supply Risk & Price Forecast 2026–2034. And if you haven't yet, catch up on the MDI/TDI shock that started it all in “MDI Price Increase 2026”.