In May last year, we asked whether the chlor-alkali challenges in East India would soon find resolution (read the original analysis here). Two threads of the same story have been running through our recent coverage.

One traces the demand side: India's aluminium sector is moving decisively downstream into Aluminum cans, and packaging, and every tonne of that growth pulls fresh investment back up the chain into primary metal and, ultimately, alumina refining.

The other traces the supply side: The chemistry and economics of the Bayer process, the regional mismatch between where caustic soda is made and where it is consumed, and the early moves by producers to close that gap. Read together, to know why Hindalco just committed ₹20,000 crore to Odisha and why that commitment matters far beyond the aluminium industry itself.

The Aditya Birla Group plans expansion of Kansariguda's plant Threefold, through its metals flagship Hindalco Industries, which has proposed an additional ₹12,000 crore (roughly USD 1.26 billion) investment in its greenfield alumina refinery at Kansariguda in Rayagada district, Odisha. The project was originally sanctioned at 1 million tonne per annum (mtpa); the revised plan takes it to 3 mtpa, lifting total project outlay to around ₹20,000 crore (USD 2.1 billion). It sits alongside Hindalco's existing 2.12 mtpa Utkal Alumina refinery in the same district, Vedanta's ongoing expansion at Lanjigarh, and NALCO's plans at Damanjodi a cluster of expansions that, taken together, is reshaping the scale of Eastern India's alumina base.

Why This Matters for Caustic Soda

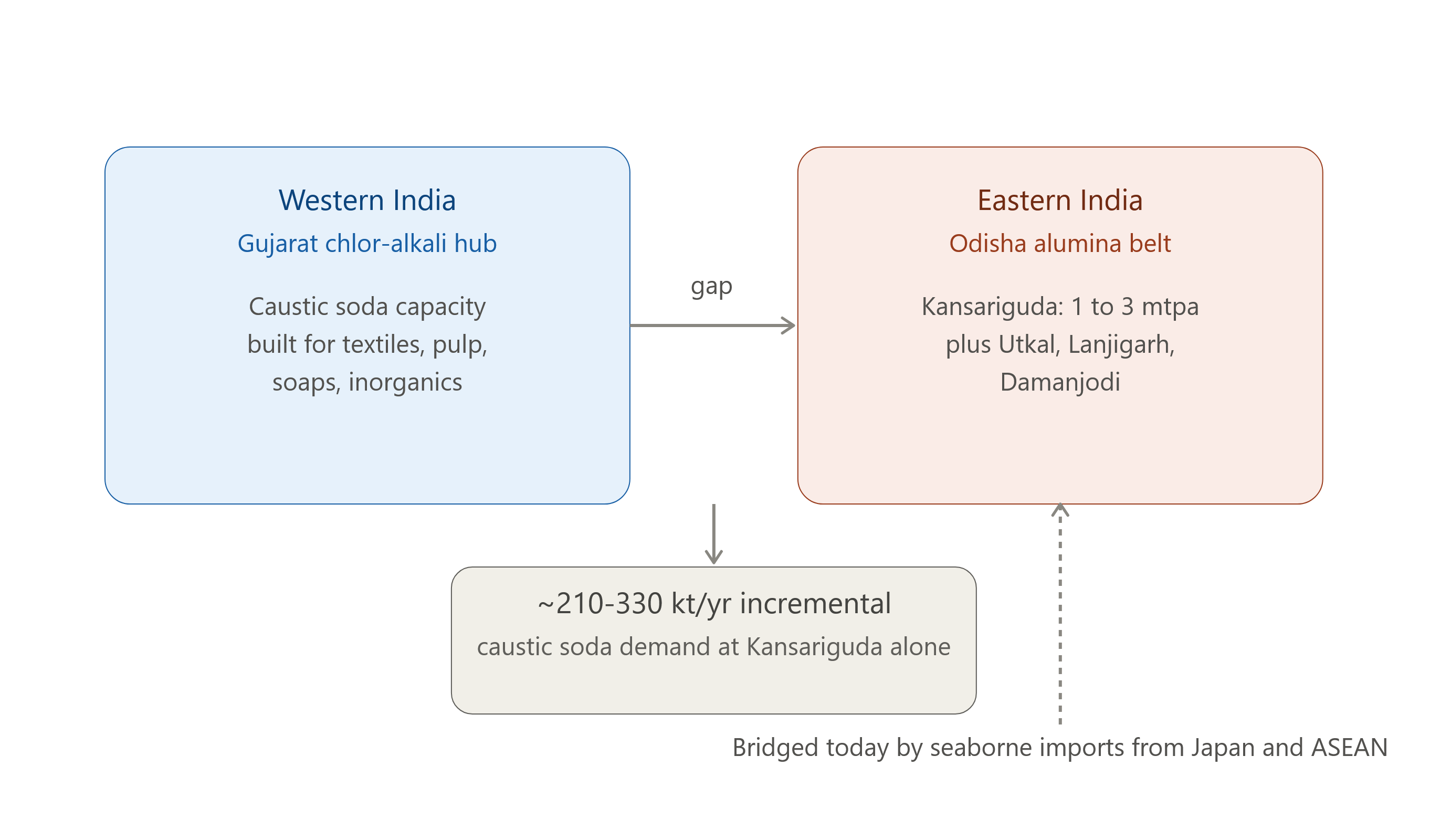

Putting a number on the Caustic Soda Gap is where the two threads meet. Caustic soda is the principal input chemical in the Bayer process, and for Odisha's gibbsite-type bauxite, consumption typically runs at 70 to 110 kg of caustic soda per tonne of alumina produced. Applied to a 3 mtpa refinery, that works out to roughly 210,000 to 330,000 tonnes of incremental annual caustic soda demand once Kansariguda reaches full capacity on its own, close to 5% of national demand. Furthermore, the parallel expansions at Lanjigarh and Damanjodi, and East India's alumina belt could plausibly be drawing close to a million tonnes of caustic soda a year by the early 2030s.

The bulk of India's chlor-alkali capacity remains anchored in Gujarat, built up over decades to serve the West's chemical industries textiles, inorganic chemicals, soaps and detergents, pulp and paper. Caustic soda lye's high-water content makes it costly to move overland, so Eastern refiners have instead leaned on seaborne cargoes from Japan and ASEAN suppliers. At the national level, India has spent recent years shrinking that reliance as supply has grown more than 10% year-on-year, import share in domestic demand has fallen below 5%, while exports are up over 30%, keeping the country a net exporter. Kansariguda's scale-up threatens to reopen that gap regionally even as it stays closed nationally, unless new capacity follows demand eastward.

The Chlorine Half of the Equation Every tonne of caustic soda arrives with almost 0.9 tonnes of co-product chlorine, and this is the piece that has historically stalled Eastern chlor-alkali projects even when caustic offtake looked attractive. East India's chlorine sinks remain thin. New vinyl and chlorinated-derivative projects from oil majors, including Indian Oil Corporation, have started to offer an outlet, but only a partial one. Any greenfield Eastern caustic soda complex will need to solve chlorine disposal through integration with PVC, chloromethanes, or similar derivatives the second half of a problem that a large, committed alumina buyer only partly solves.

How Producers Are Already Responding?

In early 2024, Gujarat Alkalies and Chemicals Ltd. (GACL) signed a memorandum of understanding with Vedanta's Aluminium business to jointly explore caustic-chlorine opportunities, whether through contractual supply arrangements or a joint venture a structure built explicitly on pairing chlor-alkali capability with alumina offtake. Kansariguda adds an intra-group twist to that logic: Hindalco's parent, the Aditya Birla Group, also owns Grasim Industries, India's largest caustic soda producer, and the group's discussions with the Odisha government reportedly already extend into chemicals alongside metals. Whether resolution comes via the GACL-Vedanta axis, a Grasim move eastward, captive units co-located with refining assets, or some combination, a demand anchor of Kansariguda's size is precisely what greenfield Eastern chlor-alkali investment has lacked until now.

Outlook

Analyze two threads side by side and the picture is consistent. Eastern India's alumina capacity is scaling faster than its caustic soda supply, downstream aluminium demand shows no sign of easing the pressure upstream, and the chlorine disposal question remains the harder half of the puzzle even as vinyl projects chip away at it. The cost of leaving the imbalance unresolved in freight, imports, and margin leakage rises with every new refinery tonne that comes online.

Locations and final investment decisions for any Eastern chlor-alkali response are still pending, but the direction of travel, and the stakes attached to it, are clearer than they have been at any point in this story so far.

This blog is a continuation of our May 2025 analysis, "Will Chlor-Alkali Challenges in East India Soon Find Resolution?" Readers may also be interested in our related piece, "India's Aluminium Can Market Is Growing. But the Bigger Opportunity Lies in Can Sheet."

For Further Information on Caustic Soda Market, Please click here

To View a Sample of Caustic Soda Market Report, Please click here

For more details on Caustic Soda Market, please contact us