Asia Pacific Liquid Crystal Polymers (LCP)

Liquid crystal polymers (LCPs) are a type of thermoplastics that show properties between highly ordered solid crystalline materials and amorphous disordered liquids over a well-defined temperature range. To date, thousands of LC polymers have been synthesized. However, only a small number have become commercially important LC materials.

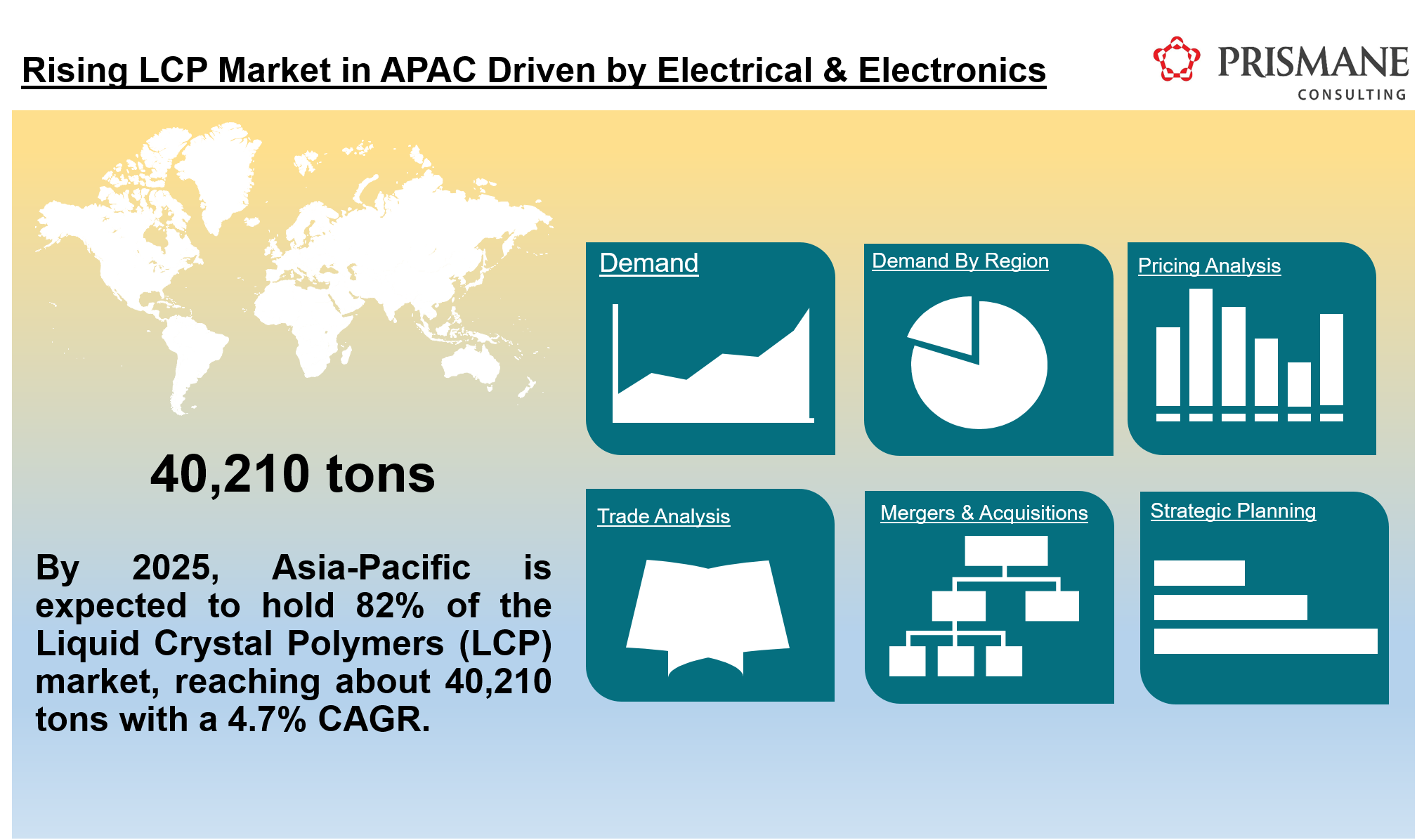

Market Overview

Asia-Pacific is estimated to be the largest consumer of LCPs accounting for over 75% of the global demand. China accounted for the major demand with strong demand from its electrical & electronics industry. Other Asian countries including Taiwan, Japan, India, Singapore and South Korea account for a decent share of global demand.

Major Liquid Crystal Polymers (LCP) Manufacturers in Asia Pacific

- Toray Industries

- Polyplastics

- Sumitomo Chemical

- Ueno

- Celanese Corporation

- Solvay

Other Manufacturers of LCP

- Untika

- Nippon Petrochemicals

To learn more about this report, request a free sample copy - Please click here

Market Trends and Forecast

By 2025, Asia-Pacific is expected to hold 82% of the Liquid Crystal Polymers (LCP) market, reaching about 40,210 tons with a 4.7% CAGR. Asia-Pacific recorded the largest demand for LCP in 2017 on account of the spur in electrical & electronics in the region. The electrical & electronics industry accounts for more than 85% of the global LCP demand in the region. The region accounted for almost 79% of LCP demand and is likely to increase its market share to around 82% by 2025 to reach about 40,210 tons. The demand in Asia-Pacific is estimated to grow at a rate of 4.7%, followed by North America at 2.5% and Western Europe at 1.9% among the major regions for LCP consumption.

Applications and Growth Drivers

In terms of LCP demand by application, the electrical & electronics industry is anticipated to dominate the Asia Pacific market. It is used as a substitute for other engineering plastics and the growing requirement for precision parts suitable for use at high temperatures will drive the growth in electrical & electronics. The advantages of LCP are excellent stiffness, flow, mechanical strength, chemical resistance, dimensional stability, and temperature resistance which makes LCP a suitable material for the rising trend of miniaturization across the electronics & electrical industry.

Rising demand from the electronics industry

LCPs are used to manufacture IC sockets, HF network switches, power modules for solar and wind converters, inverters, electrical connectors, and other electrical devices. The increasing demand of microinjection molding is anticipated to drive the LCP market growth.

The growing demand for connectors with high pin density is anticipated to drive LCP demand in the forecast years. Further, the increasing demand for lightweight and high-performance materials from the automotive industry to produce fuel-efficient vehicles is projected to present huge market growth opportunities.

LCPs are also used in electronic components for robots, satellites, digital cameras, headphones, printers, etc. The remaining demand is from the automotive, industrial, and medical industries.

To learn more about this report, request a free sample copy - Please click here